Credit Reports

When you want to set up a credit card account, you are asking the bank to approve making you a loan. Any purchase made on the credit card is basically a loan from the bank that the cardholder will repay when paying the credit card bill. That is why to approve a credit card for anyone, the bank must check the potential cardholder’s financial history.

The bank might ask several the following questions:

1. How much money do you earn?

2. Do you have other credit cards? What kind of balances do you have on them?

3. Have you ever declared bankruptcy? Bankruptcy is a legal term used when a person cannot repay his debts.

4. How old are you?

5. How long have you had your current job?

6. Do you own your house?

7. What is your social security number?

8. Will you approve a “credit report” of your credit history?

Each of these questions is designed to help the bank decide if a client is “credit worthy.” This means they need to learn enough about any potential cardholder to ensure that extending credit to the cardholder will be a good investment for them.

If they approve a credit card, they are really approving making a loan of whatever credit limit is on the card. If they approve a credit limit of $2,000, then they are saying the client can use the credit card to make charges totaling $2,000.

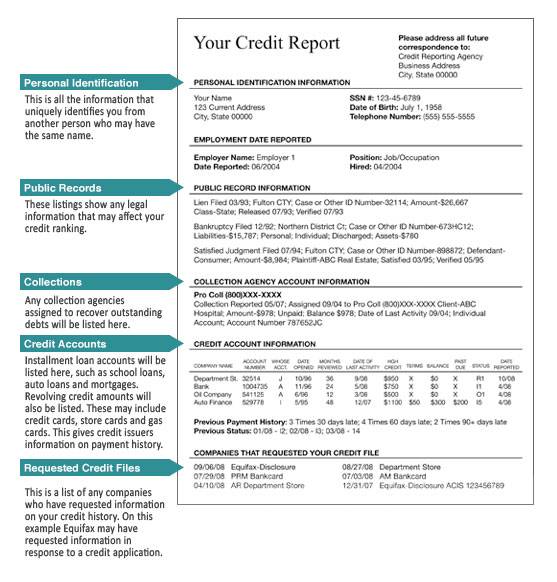

The reason that the bank or credit union asks for a social security number is so that it may obtain a credit report. The credit report will list the different type of assets the client has, as well as detail any times loans have not repaid in a timely manner. That means every time consumers obtain a credit card, debit card, or checking account, they are building up a credit history. This credit history then becomes part of the credit report that the financial institution or lender will use when deciding if they will approve a loan or credit card. The lender will then get the consumer’s credit score from the different credit rating agencies. The credit score will enable the bank to decide if they think the customer is a good credit risk or not. So approval for the loan and the interest rate charged are determined by the credit score. Generally, the higher the credit score, the lower the interest rate. That is why it is so important to maintain a positive credit history.

According to www.consumer.ftc.gov, the Fair Credit Reporting Act (FCRA) requires each of the nationwide consumer reporting companies — Equifax, Experian, and TransUnion — to provide you with a free copy of your credit report, at your request, once every 12 months. The FCRA promotes the accuracy and privacy of information in the files of the nation’s consumer reporting companies. The Federal Trade Commission (FTC), the nation’s consumer protection agency, enforces the FCRA with respect to consumer reporting companies.

A credit report includes information on where you live, how you pay your bills, and whether you’ve been sued or arrested, or have filed for bankruptcy. Nationwide consumer reporting companies sell the information in your report to creditors, insurers, employers, and other businesses that use it to evaluate your applications for credit, insurance, employment, or renting a home.

Time limits for keeping negative financial information:

The three credit-reporting agencies mentioned above can report a consumer’s most accurate negative information for seven years and bankruptcy information for ten years. However, there is no time limit on reporting information about criminal convictions.

Why do you need a positive credit history?

You need to pay your bills on time, otherwise your credit report might not be positive. If you have trouble paying your bills on time, the credit agencies will report that you are not as good a risk. In that case, you might have to pay a higher interest rate when you apply for a loan or credit card or be charged a higher deposit for services. If you have a great credit report, a positive credit history will mean a higher credit score from the reporting agencies.

This has several benefits. First, a high credit score makes it easier to get a credit card or debit card. Second, it qualifies consumers for lower interest rates when they are approved. Finally, it enables people to qualify not only for credit cards but also for loans such as for a car or a house.